Shocking: The merger between a lingerie e-commerce brand and a Chinese EV startup has a few red flags

Shocking: The merger between a lingerie e-commerce brand and a Chinese EV startup has a few red flags

Did some digging into the $NAKD merger with Cenntro Auto. It's a shit show.

***BREAKING: RVC RESEARCH DOWNGRADES $NAKD, PT: $0

Overview

Naked Brands and Cenntro Automotive are merging.

Cenntro CEO Zugang Wang, AKA Peter Wang, has taken multiple companies public through reverse mergers, none of which were in the least bit successful.

Peter Wang was sued for defrauding an investor in Cenntro in 2012.

Naked Brands and Cenntro have misled investors on the state of the company, and have failed to disclose related party transactions involving entities controlled by Peter Wang.

Cenntro claims to be a leader in automated intelligence and self-driving vehicles, but has almost no patents for such technology.

This is a shitty stock promotion.

Naked Brands

In the year of our Lord two thousand and twenty-one, nothing in the capital markets is surprising anymore. I do not think our society is benefitting from multiple zero-revenue electric vehicle companies going public at multi-billion dollar valuations. Anyway.

Naked Brands was founded in 2010 in Vancouver as a men’s underwear manufacturer. The company is now based in New Zealand. Over the past decade, the company expanded into women’s underwear, lingerie, apparel, etc. In January 2021, the company announced it would be spinning off its retail unit to focus solely on e-commerce. This was right before the Great Short Squeeze of 2021, and Naked’s stock price increased from $0.19 per share to $3.25 in about a month. Management took advantage of the high share price and completed multiple equity offerings during the year. The company now had $280 million burning a hole in its pocket and was searching for something to do with it. In their words:

“We intend to pursue accretive, strategic acquisitions with synergistic benefits that complement our business and operations and help us expand our brands, categories, product offerings and geographies.”

Naturally, that lead to Naked announcing on November 8th, 2021 that the company would be acquiring electric vehicle startup Cenntro. Naked was supposed to be delisted from the Nasdaq in October due to the stock’s minimum bid being below $1.00 for 10 consecutive trading days. But the company received a 180-day extension. On December 21, 2021, the company held an extraordinary general meeting where shareholders approved both a 15:1 reverse split and the Cenntro merger.

Transaction Highlights:

All-stock deal in which Naked will issue roughly 2.5 billion shares to Cenntro, whose shareholders will own 70% of the combined company. NAKD shareholders will own the other 30%. Implied valuation of Cenntro is about $1.7 billion.

Of the 70% that Cenntro controls, CEO Peter Wang will beneficially own about 26% of the combined company.

Naked is required to have more than $282 million in cash and less than $10 million of liabilities at the time of closing. NAKD must be trading on the NASDAQ at the time of closing.

A $30 million secured loan to Cenntro.

NAKD to discontinue the remaining lingerie business after the merger.

The new company is expected to start trading on the NASDAQ, pending their approval, under the ticker $CENN on December 30, 2021.

Update 12/30: NASDAQ approved the merger today. The ticker will remain $NAKD for now.

Cenntro

Cenntro was incorporated in Hong Kong in 2011. According to their website, Cenntro is led by Peter Wang, “a visionary entrepreneur”.

The Company is a designer and manufacturer of electric light- and medium-duty commercial vehicles (“ECVs”). The Company both (i) designs, manufactures, assembles, homologates and sells ECVs to third parties for distribution and service to end-users and (ii) distributes manufactured vehicle kits, which are then assembled, homologated, sold and serviced by third parties in their respective markets.

Look at all the customization options!

Cenntro has big plans after this merger, including expanding production to three new countries in 2022 and developing nine new EV models by 2024. The company has announced the plan to invest $25 million into a 100,000 square foot facility in Jacksonville, FL that will open next year and produce over 50,000 vehicles annually.

Cenntro, since its formation in 2011, has produced and sold approximately 3,300 units of one model, the Metro. The Metro was not developed by Cenntro. The IP was acquired from STIL-Brandt Motors, a French automaker that Peter purchased out of bankruptcy for €8 million in 2014. STIL’s version of this car was called the Citelec:

Metro:

The SITL acquisition was a good one for Cenntro. The factory never produced a single car during Cenntro’s ownership. Peter allegedly paid $10 million in out-of-pocket expenses over the 16 months he owned the factory. Sometime in 2015, Cenntro Automotive France was placed in receivership by a French court, all of the employees were laid off, and shortly thereafter the subsidiary was sent to liquidation.

In 2014, Cenntro also announced the company was launching a production facility for the Metro vehicles in Sparks, Nevada, where the company was to receive $1.2 million in tax deferrals and grants. Besides this press release and a few other local news articles announcing the opening of the factories, I cannot find any other info on what happened there, which leads me to believe there were no vehicles ever produced there either.

It was not easy to find information on the company’s history between 2014 and 2021. I had to really grind for this stuff. This is their official Twitter account:

Two of their old websites are gone. Their US website, cenntromotors.com, went down sometime in 2017. Their business lines back then apparently included renewable energy, water treatment and precision manufacturing!

Their China website, cenntroauto.cn/en, went down near the end of 2020.

In 2017, the company announced a “smart manufacturing platform.”

According to Hengyuan Automobile, Rongda Intelligent Manufacturing is a new energy automobile manufacturing platform, covering design, R&D, parts, assembly, process, operation, capital and other related factors, and aggregates 4 technology research institutes and 9 automobiles. An industrial co-operation body including assembly plants and more than 150 parts suppliers.

No idea what that was supposed to mean, lost in translation I guess. At this event, Cenntro also introduced two new prototypes, the Neibor and the Altera.

These vehicles never entered production. The following year, Cenntro announced the Metro II, the new and improved edition of their flagship vehicle, and also a “self-driving vehicle chassis.”

Their self-driving vehicle was expected to be released in the Fall of 2018, which, shockingly, did not happen. The company claims to have tested this fully autonomous vehicle around the same time in the streets of Shengzhou City, China. I was unable to find any evidence of said test.

Just today, Cenntro announced delivery of the first units of their second model, the Logistar, which is designed for the EU market.

The company has delivered 628 Logistar units in December. The company also reaffirmed their guidance for 20,000 vehicle sales next year (lol).

Bet on the jockey, not the horse…

is a classic investing saying. I do not think you should do that here.

Peter Wang is the CEO of Cenntro. Peter is also the Chairman of another public company, Greenland Technologies (NASDAQ:GTEC).

Peter was born in China before moving to the United States to attend college. Peter worked at AT&T Bell Labs from 1987 to 1990. Peter then went on to start Unitech Telecom, renamed UTStarcom, where he worked from 1990 to 1995. This company was one of the first Chinese companies to list on the NASDAQ. They were charged by the SEC in 2008 for violating federal securities laws relating to accounting, and again in 2009 for violating the Foreign Corrupt Practices Act by bribing Chinese officials with company resources. Peter had left the company before that, though.

Peter has run a few public companies over the years. Peter is a fan of a listing technique known as a reverse merger. Remember the China Hustle? A decade ago, hundreds of Chinese companies went public on US stock exchanges through reverse mergers, where a private company merges with a public shell company. Like a SPAC deal but before it was called that. A large percent of these companies were frauds and these companies destroyed tens of billions of dollars of investor capital.

Peter’s next venture after his exit from UTStarcom was China Quantum Communications. China Quantum went public through a reverse merger with shell company Techedge (OTCBB: TEDG) in 2004. The company did telecom stuff like providing telephone services between US and Chinese citizens from 2004 to 2006. Then in 2006, Techedge announced that they would continue their current telecom activities while also pivoting to biopharma. Like making vaccines. Peter was bullish on their pivot:

It turns out the company was not a top vaccine producer:

During their expansion into biopharma, CBPC issued an 8% convertible note to investors. The monthly interest payment on this note was payable in shares. The company defaulted on these notes in less than a year, and then defaulted again when the notes matured in 2008. From 2006 to 2009, the company managed to issue over 600 million shares of their stock, mostly to pay the noteholders.

Over the life of the company, China Biopharma lost $15.8 million. More info about this company can be found in their last 10-Q from May 2009. The company received numerous inquiries from the SEC regarding their filings. In one from 2005, the SEC asked CBPC how many shares of the company Peter beneficially owned. The SEC’s final letter to CBPC, addressed to Peter in June 2009, asks some important questions public companies usually answer in their filings, such as:

“Where did your company get $2.1 million to buy out that joint venture?”

“How did you recognize revenue over the past three years?”

“Why was there $0 of inventory reported on your balance sheet?”

Two months later a follow-up letter to the company was sent. China Biopharma simply did not respond to this and never made another filing with the SEC again. Around this time Peter moved back to China to work on other projects. CPBC somehow traded on the OTC markets until 2017 when the SEC revoked their securities.

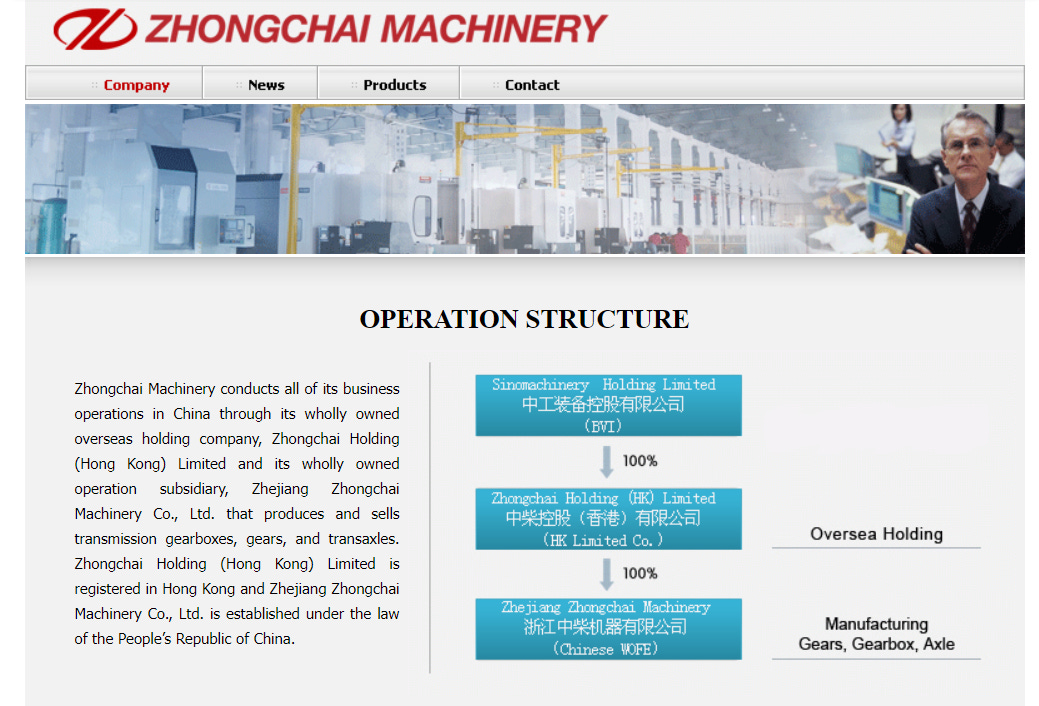

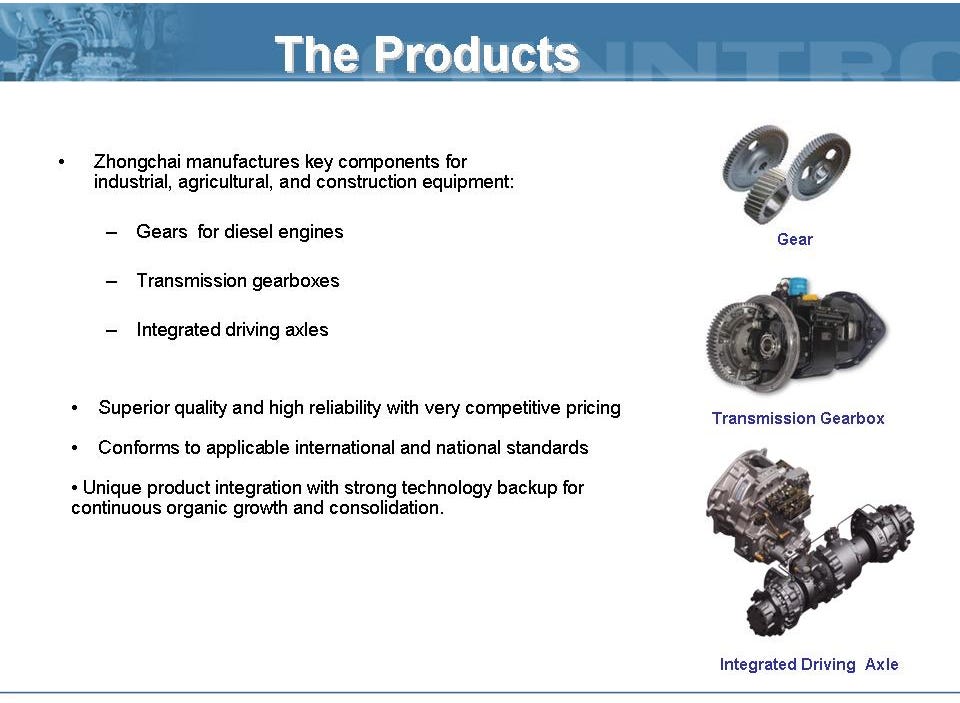

Zhejiang Zhongchai

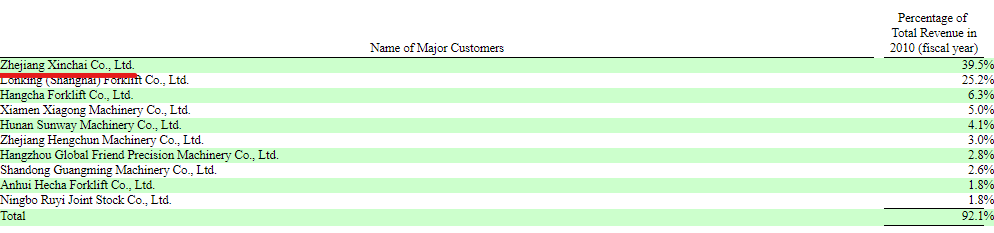

Peter’s next business venture in the US markets was a company called Unsunco, which went public through a reverse merger with a shell company called Equicap (OTCBB: EQPI) in March 2007. Peter was the Chairman, President, and CFO of Unsunco. Unsunco owned a 75% interest in a company called Zhejiang ZhongChai Machinery Co., Ltd. (ZhongChai), which in turn owns all of Zhejiang Shengte Transmission Co., Ltd (Shengte), which produces gearboxes and transmissions for industrial equipment like forklifts. By 2010, the China Hustle was in full swing, and Zhongchai was looking to capitalize by uplisting to the NASDAQ. The company created an investor presentation to pitch the company to new investors:

In 2010 the company had its best year yet, doing $10 million in sales and $1 million in net income. 39.5% of those sales came from one company called Zhejiang Xinchai.

Zhongchai and Xinchai entered a JV agreement for the distribution of Zhongchai’s products in 2007.

Zhongchai never made it to the NASDAQ. The company went the way of China Biopharma and was taken private and delisted. As you can see on their old website, Xinchai (also known as Sinomachinery) acquired Zhongchai in 2011 and made Peter the CEO of the combined company.

Sinomachinery then raised money from a group of PE funds in 2011, including Sequoia Capital China and Welkin Capital.

In 2014, Sinomachinery was…acquired by Cenntro?

Odd for an up-and-coming electric vehicle startup to purchase a company that produces diesel engines and transmissions for industrial machinery.

Greenland Technologies (NASDAQ: GTEC)

Fast forward to 2019, and Zhongchai is making its return to public markets through a merger with the SPAC Greenland Acquisition Corp. Peter is the Chairman of the Board of Directors and his son, Raymond Wang is the CEO. Cenntro was the selling shareholder and Peter owns 59% of Greenland through Cenntro.

The company was brought public at an implied enterprise value of $101 million:

Zhongchai’s primary business has not changed, the company still sells transmissions and drivetrains.

2010:

The Company started to produce and deliver transmission gearboxes in 2008. Since then it has sold 92 sets, 1767 sets, and 9,924 sets of transmission gearboxes during the fiscal years in 2008, 2009, and 2010 respectively

2019:

Business has really picked up!

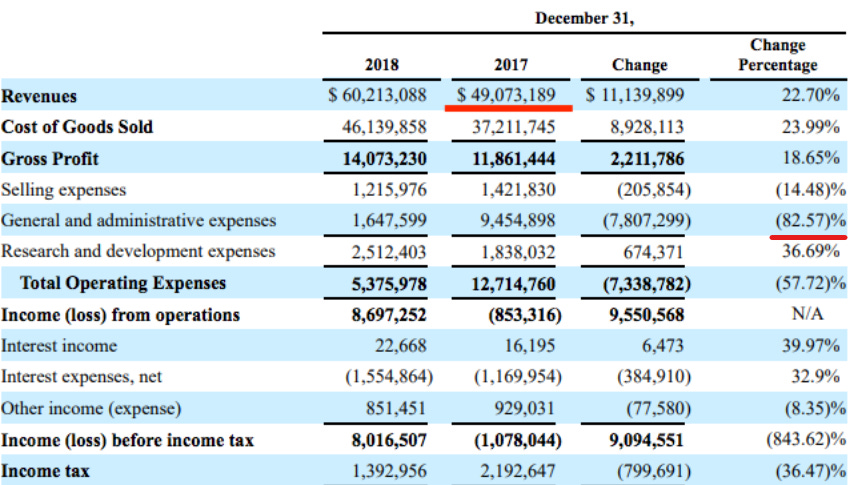

Impressive when a company’s sales grow by 22% in a year while general and administrative expenses decreased by 82%! Their explanation is:

And even more so for a manufacturing company to do $50 million in sales with no plant or buildings on their balance sheet:

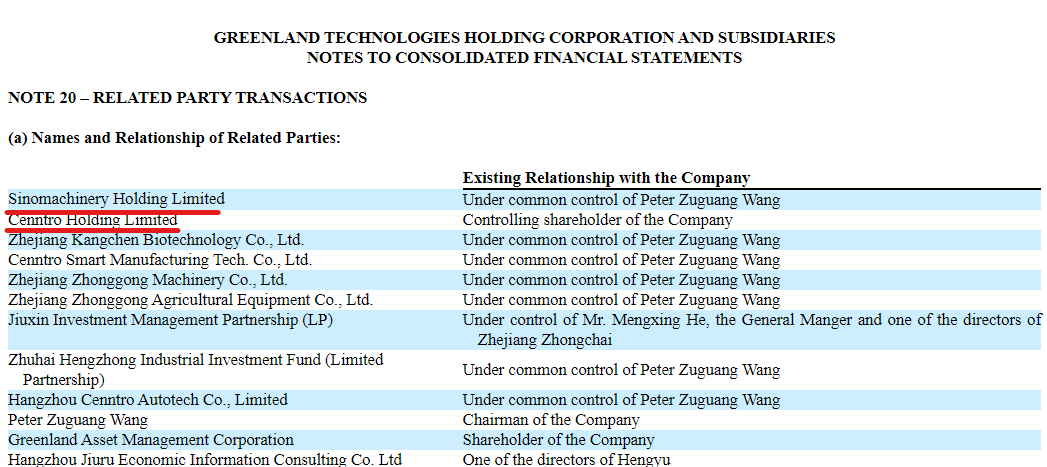

Greenland/Zhongchai’s related parties include Sinomachinery and Cenntro.

Reviewing the ensuing related party transactions is where this blows up. Will revisit that in a minute.

Where are the orders?

According to their investor presentation, this is management’s expectation for Cenntro’s sales:

Lol

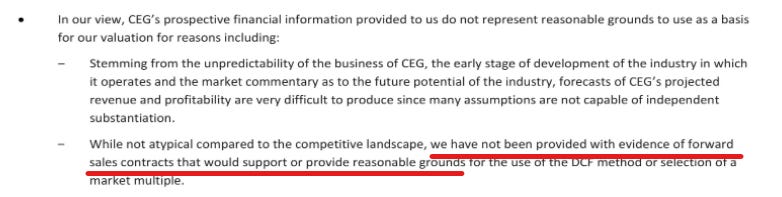

Cenntro’s financials can be found at the end of their proxy statement. These were prepared by FTI Consulting Australia, who wrote the fairness opinion. Additional information was taken from this Form 6-K.

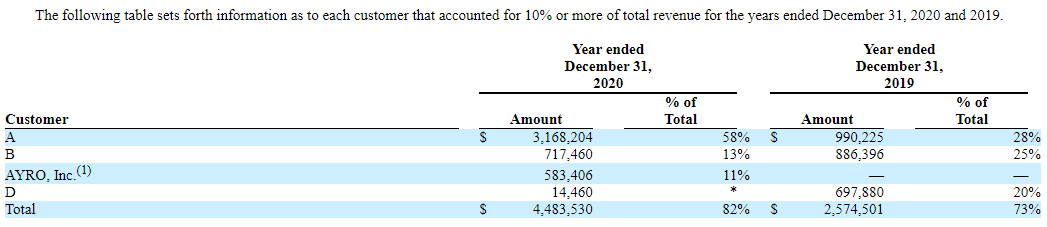

Their top three channel partners accounted for nearly all of Cenntro’s revenue over the past two years:

We can assume customer A is Tropos motors and B is Upsilon:

One of these three channel partners canceled their agreement with Cenntro in 2020:

The company claims to have a backlog of over 1,000 orders. But Cenntro was unable to provide FTI with any evidence of sales contracts for said orders.

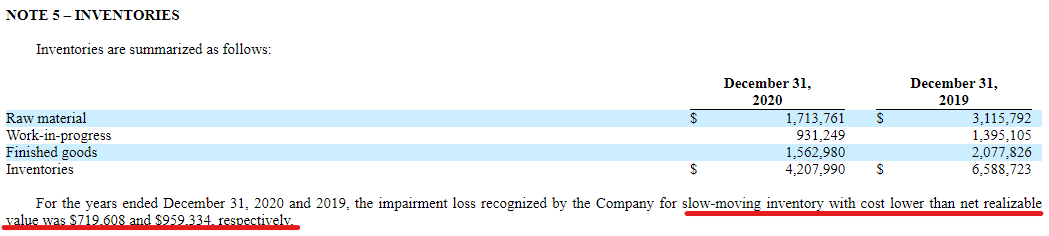

Why did Cenntro write down slow-moving inventory in 2020 if there was a backlog of orders? The company is only selling Metro vehicle kits and vehicles at this point.

Naked loaned Cenntro money for the opposite reason:

Naked Brand Group has also provided Cenntro a $30 million secured loan to provide additional working capital to meet its substantial backlog during the pendency of the Transaction.

Why is that?

On November 29, the company announced a 2,000 vehicle order from HW Electro, one of their distribution partners in Japan. This was after the merger/loan with Naked was announced and a week after the FTI fairness opinion was dated.

Peter has lied about Cenntro’s order numbers before:

Statistics show that in 2017, Rongda Zhizhi [Cenntro] sold 2,085 vehicles throughout the year, and this year has already received orders for 40,000 vehicles, a growth rate of 20 times.

It is safe to say that Cenntro did not sell 40,000 vehicles in 2018.

Cenntro is insolvent

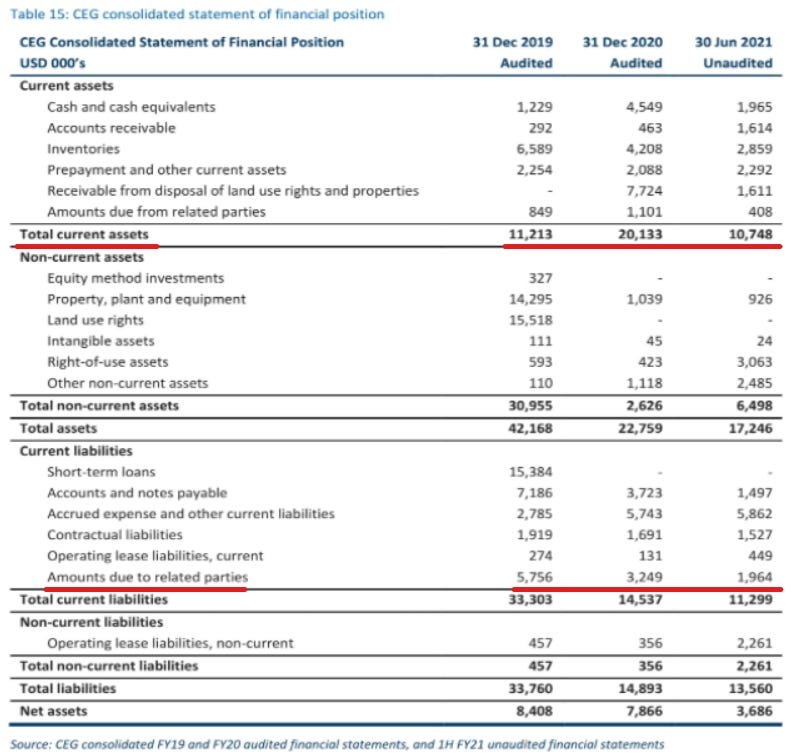

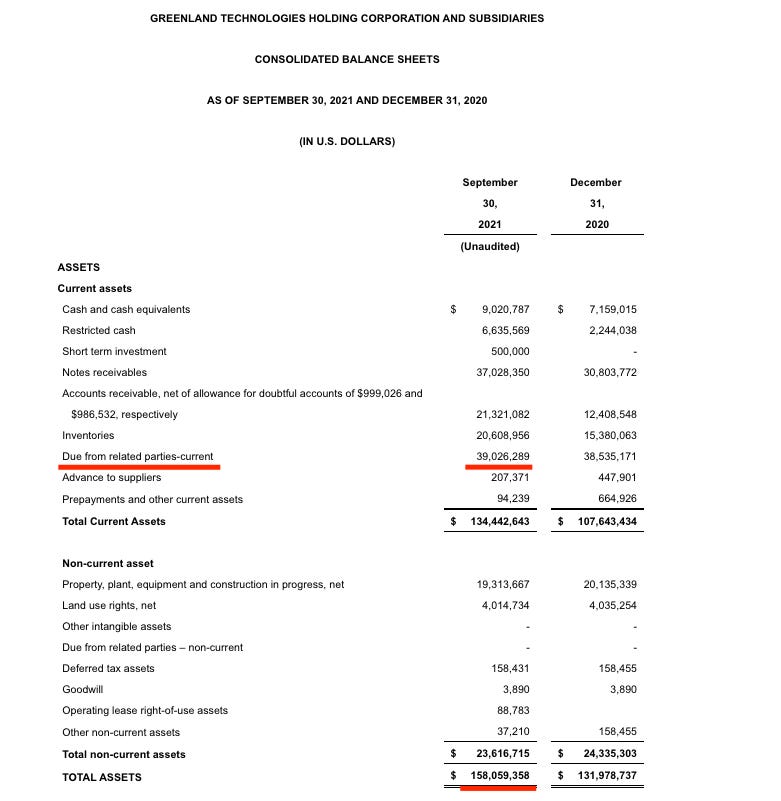

Back to the related party transactions. See the balance sheet:

And the NAKD/Cenntro pro forma balance sheet:

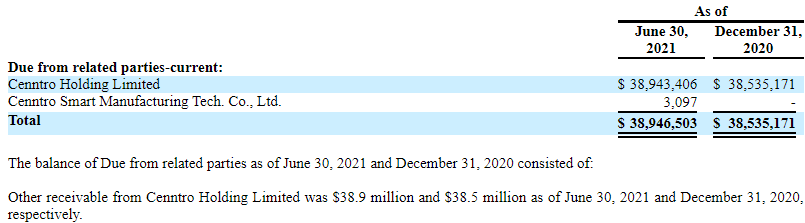

Cenntro owes $1.964 million to related parties. So what?

This amount is understated by about $39 million, which Cenntro owes Greenland from a previous transaction. I am not sure how NAKD/FTI/the SEC missed this, as it is disclosed in dozens of Greenland’s filings:

What is Hengyu? A shell company. Why is it a part of Greenland?

Confusing!

This transaction was mentioned in the Sinomachinery/Xinchai offering documents. Sorry it is in Chinese, I could not find an English translation. Xinchai was spun out from Sinomachinery and listed on the Shenzen Stock Exchange earlier this year. Sinomachinery was supposed to list shares in Hong Kong in 2013. This did not work out because the company could not get a valuation high enough to pay off the PE investors. Instead, Hengyu was incorporated to buy back the PE fund’s preferred shares at cost:

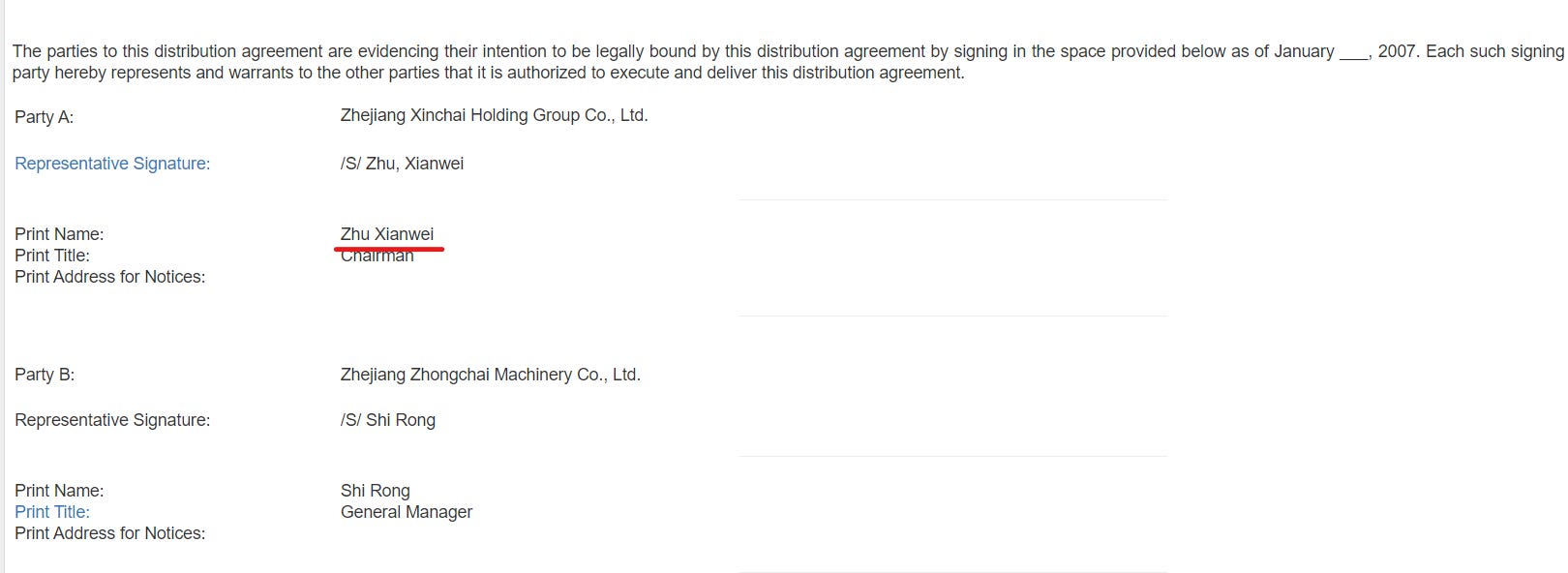

In September 2015, Zhu Xianwei and Guo Min (who held equity for Wang Zuguang) jointly established Shanghai Hengyu. Shanghai Hengyu was established only as a channel to return the investment funds of overseas preferred stock investors and did not engage in specific business operations.

On September 15, 2015, Zhu Xianwei, Wang Zuguang, Shanghai Hengyu and the overseas preferred stock investors SCC investors, MK investors, Professional Journey Limited, and Welkin Machinery signed the "Share Purchase Agreement", agreeing that Shanghai Hengyu will purchase shares of China National Industrial Equipment Group [Sinomachinery]. The share purchase price is paid in two installments, with a total consideration of US$50 million.

To summarize, Hengyu (controlled by Peter) bought back preferred shares issued by Sinomachinery (controlled by Peter) in 2015 for $50 million. Then in 2017, Hengyu, now a subsidiary of Zhongchai (a company controlled by Peter) sold these preferred shares to Cenntro (a company controlled by Peter) for approximately $36 million, plus interest, to be paid in 2020. The outstanding balance of this sale was never been paid from Cenntro to Zongchai/Greenland/Hengyu. Sounds like a word that rhymes with Fonzi.

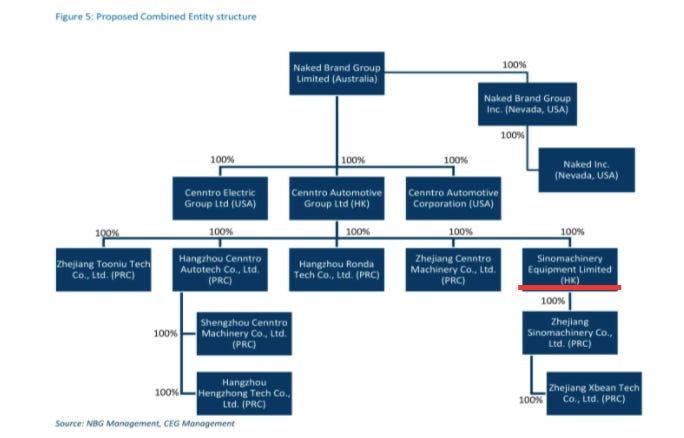

Here you can see where Sinomachinery fits into the Cenntro umbrella of entities that NAKD will be acquiring:

Sinomachinery, previously a manufacturer of diesel engines for industrial equipment, is now developing a whole ass electric vehicle.

On October 2, 2020, Greenland filed an interesting Schedule 13D:

On December 13, 2019, Welkin Machinery Investment I, L.P (“Welkin”) entered into a share purchase agreement with Mr. Peter Wang, pursuant to which Welkin agreed to cancel the indebtedness of Sinomachinery Group Limited (“Sinomachinery”) to Welkin in the amount of US$2 million in consideration for 193,051 Ordinary Shares of the Issuer. Sinomachinary is a related party of the Issuer as both entities are under common control by Peter Zuguang Wang, the Issuer’s controlling shareholder and chairman of the board of directors. On October 2, 2020, Peter Zuguang Wang, through Cennto Holding Limited, transferred 193,051 Ordinary Shares to Welkin.

Cenntro, which owns 7.5 million shares of Greenland, granted $2 million worth of those shares to Welkin, one of the PE firms that invested in Sinomachinery in 2011 to cancel their debt. A few questions:

Why did Sinomachinery need to cancel its debt to Welkin?

Why did Cenntro pay Welkin in Greenland shares?

Is this merger being used to bail out Peter Wang’s previous bad deals?

The $39 million payment from Cenntro to Greenland was due on October 27, 2020. On October 27, 2020, the payment was not made. The due date was extended by an agreement between Peter and his son, Raymond Wang (CEO of Greenland) until April 2022.

Why did Cenntro not make this payment? Looking at their balance sheet, this liability is greater than the company’s total assets when the payment was due.

Cenntro has been insolvent for the entire term of the financial statements presented to investors (and probably before then, too). Cenntro is now being bailed out by the shareholders and investors of Naked Brands. There is zero chance that Peter Wang is unaware of this, as he signed off on the agreement to extend the due date of Cenntro’s payable/Greenland’s receivable.

But wait, there’s more!

Greenland fired two different auditors in 2020:

“On January 6, 2020, the Board of Directors of the Company (the “Board”) approved the dismissal of Marcum LLP (“Marcum”) as the Company’s independent registered public accounting firm, effective January 6, 2020.”

“On November 13, 2020, the Board approved the dismissal of BDO China Shu Lun Pan Certified Public Accountants LLP (“BDO”) as the Company’s independent registered public accounting firm, effective November 13, 2020.”

Commissioners:

We have read the statements made by Greenland Technologies Holding Corporation under Item 4.01 of its Form 8-K dated November 17, 2020. We agree with the statements concerning our Firm in such Form 8-K; At the time of our dismissal, we were in the process of evaluating the recoverability of the related party receivable from Cenntro Holding Limited and such procedures have not been completed. We are not in a position to agree or disagree with other statements of Greenland Technologies Holdings Corporation contained therein.

Very truly yours,

BDO China Shu Lun Pan Certified Public Accountants LLP

That’s right. Greenland fired BDO while the auditors were determining if Cenntro was going to be able to pay Greenland the $39 million. That sounds like something a company would do to hide the fact that their other company was not able to pay $39 million.

That is 25% of Greenland’s total assets on the balance sheet, assuming everything else there is real. And in only a few days, Peter will have access to $282 million to keep this related-party shell game going. This could actually be the next Tesla!

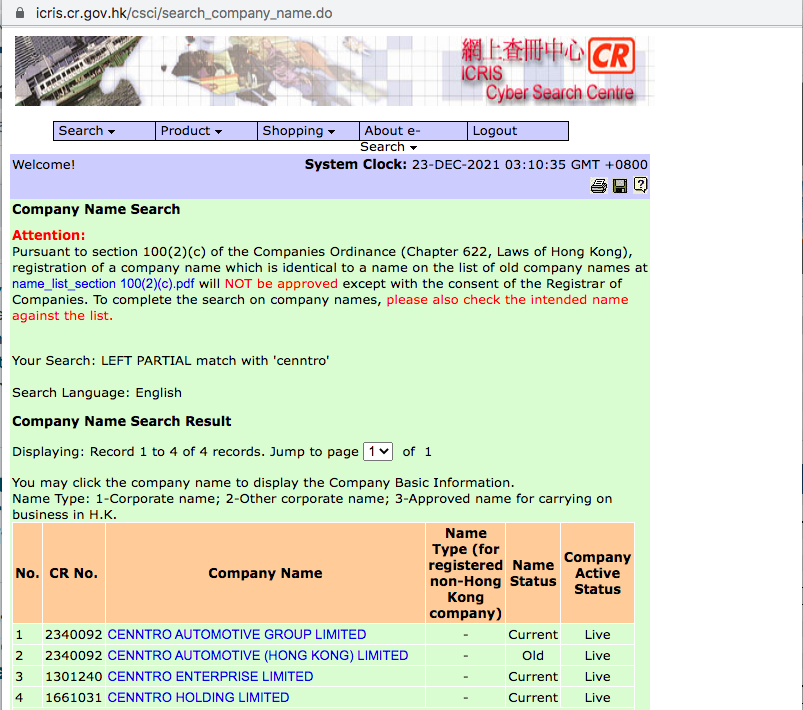

Update 1/2/22: Cenntro Holding Limited is not listed as a reporting entity under Cenntro Automotve Group. Cenntro Holding is owned by Cenntro Enterprise Limited, which is controlled by Peter Wang. Cenntro Holding is the principal stockholder of Cenntro Auto and Greenland. It is unclear whether Cenntro Holding was a part of Cenntro Auto before 2020.

Here is a timeline of these events.

2007 – Zhongchai goes public in the US.

2007 – Zhongchai and Xinchai establish joint venture.

2011 – Zhongchai taken private/delisted.

2011 – Xinchai changes name to Sinomachinery.

2011 – Zhongchai is acquired by Sinomachinery.

2011 – Cenntro is incorporated.

2011 – Cenntro acquires Sinomachinery/Zhongchai.

2014 – Cenntro acquires SITL.

2015 – Hengyu buys out Sinomachinery’s PE investors for $50 million

2017 – Cenntro buys Sinomachinery from Hengyu (subsidiary of Zongchai) for $35 million, to be paid back with interest in 2020.

2019 – Zhongchai spun out from Cenntro and merged with Greenland Acquisition.

October 2020 – Cenntro fails to make payment to Greenland/Zhongchai for the acquisition of Sinomachinery. Cenntro and Greenland agree to extend the due date until April 2022.

November 2020 - Greenland fires their auditor, BDO China, while it is evaluating the related party payment from Cenntro.

December 2020 – Cenntro pays Welkin (PE Fund) in Greenland/Zhongchai shares to forgive Sinomachinery’s debt.

2021 – Xinchai is no longer a part of Sinomachinery and is listed on the Chinext exchange.

November 2021 – Cenntro and Naked Brands announce merger.

Patents

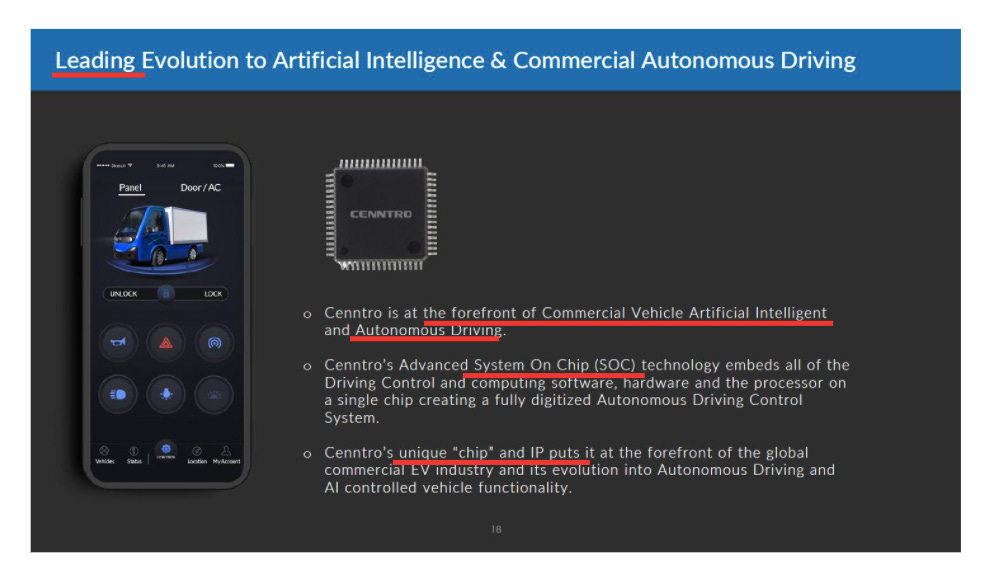

Cenntro claims to have a lot of intellectual property that will make the company a leader in AI, internet of things, autonomous driving, crypto, NFTs, flying cars and whatever else:

You get the point.

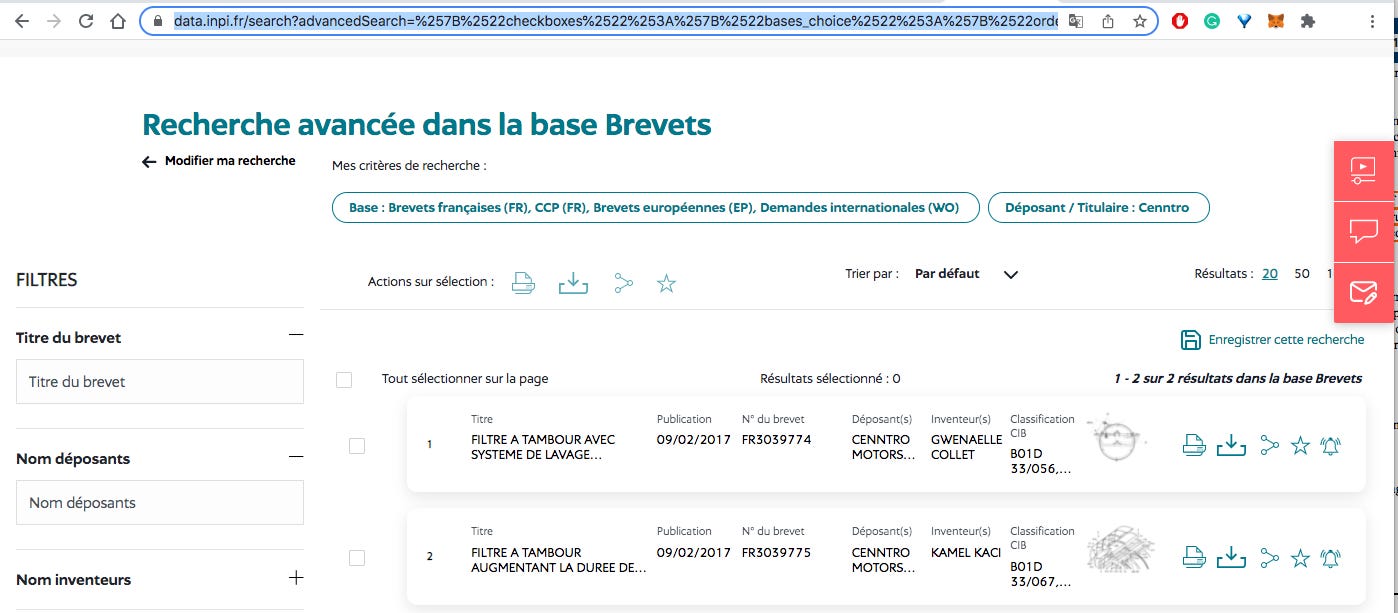

I did some patent searching and the following is what I found. In France, Cenntro has two patents. They are for drum filters:

Cenntro and Sevic, a European EV startup, established a joint venture to manufacture Metro vehicles in Bulgaria in 2018. Sevic is now working with another company to manufacture these vehicles in Europe, and acquired all of Cenntro’s European IP for the Metro in 2019.

In the United States, Cenntro has zero patents:

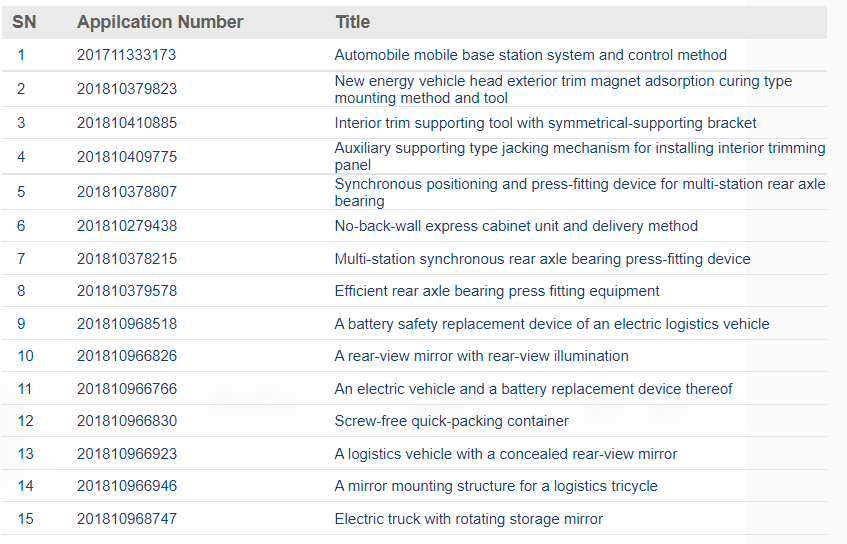

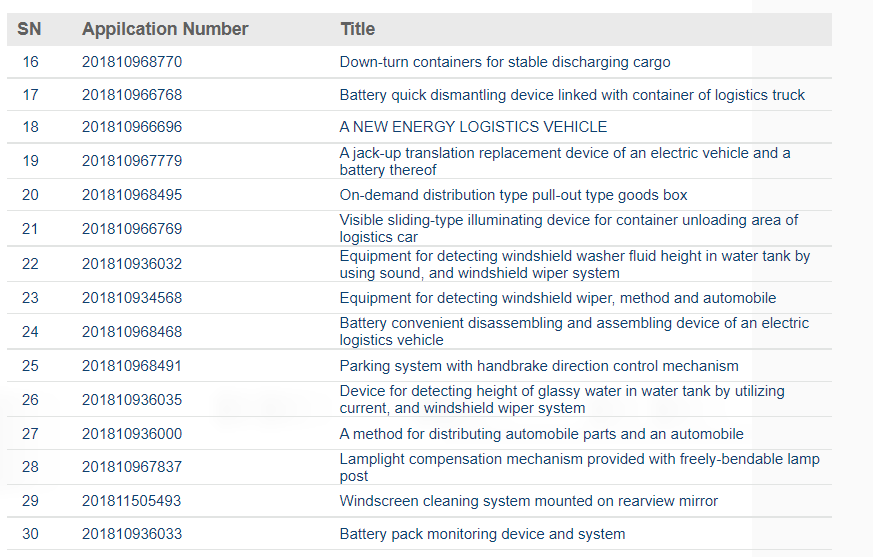

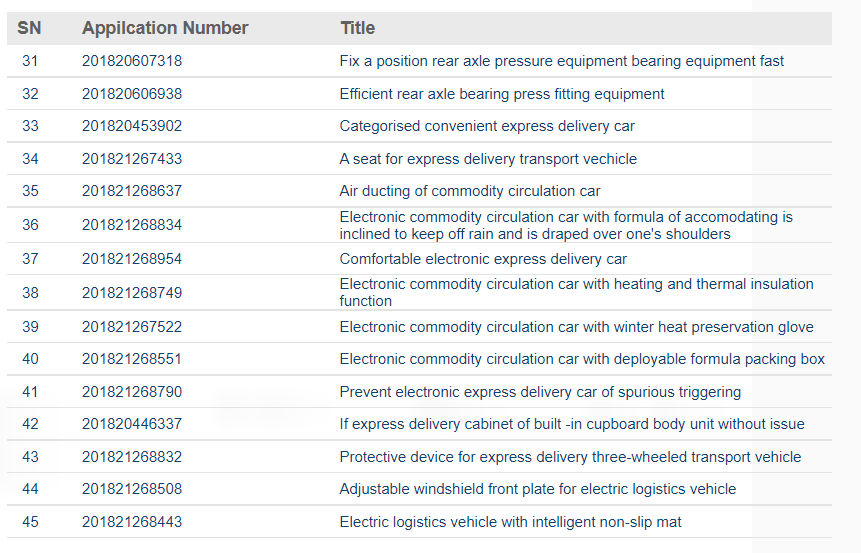

I went through the China IP search system for Cenntro and all of its subsidiaries. The following is the list of them:

Starting with the subsidiaries in China that have a combined total of zero (0) patents:

Zhejiang Cenntro Machinery Co.

Zhejiang Sinommachinery Co.

Hangzhou Cenntro Autotech Co.

Hangzhou Hengzhong Tech Co.

Hangzhou Ronda Tech Co.

Zhejiang Tooniu Tech Co.

Zhejiang Xbean tech Co.

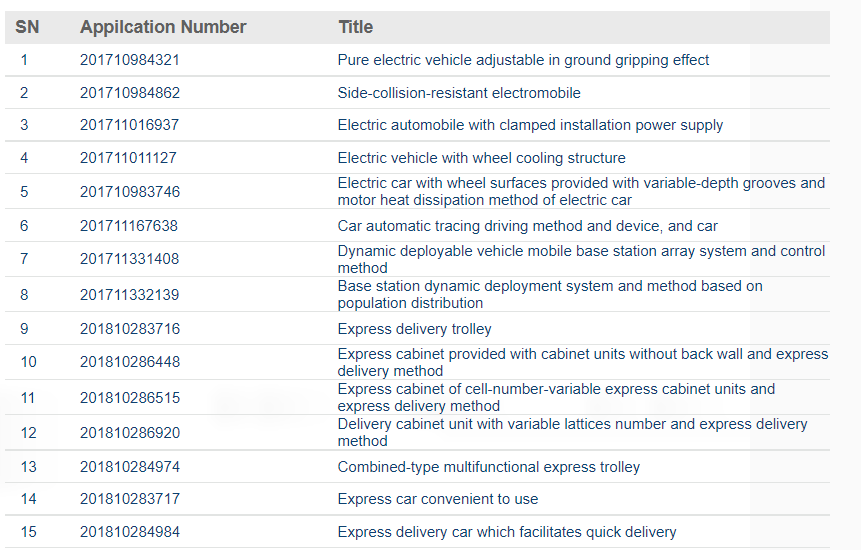

Cenntro has 46 patents:

Here’s one for an automobile control method (it has nothing to do with self-driving):

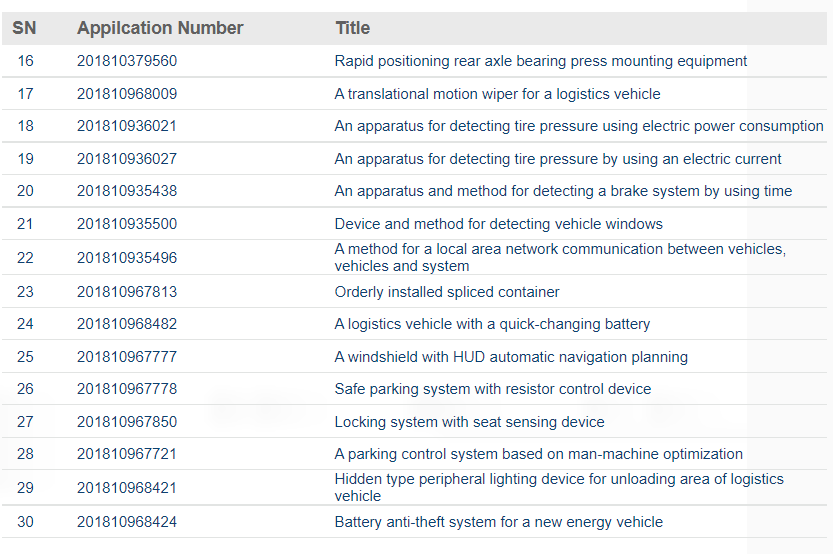

Hangzhou Rhonda Zhizhao, a subsidiary of Cenntro, has 53 patents:

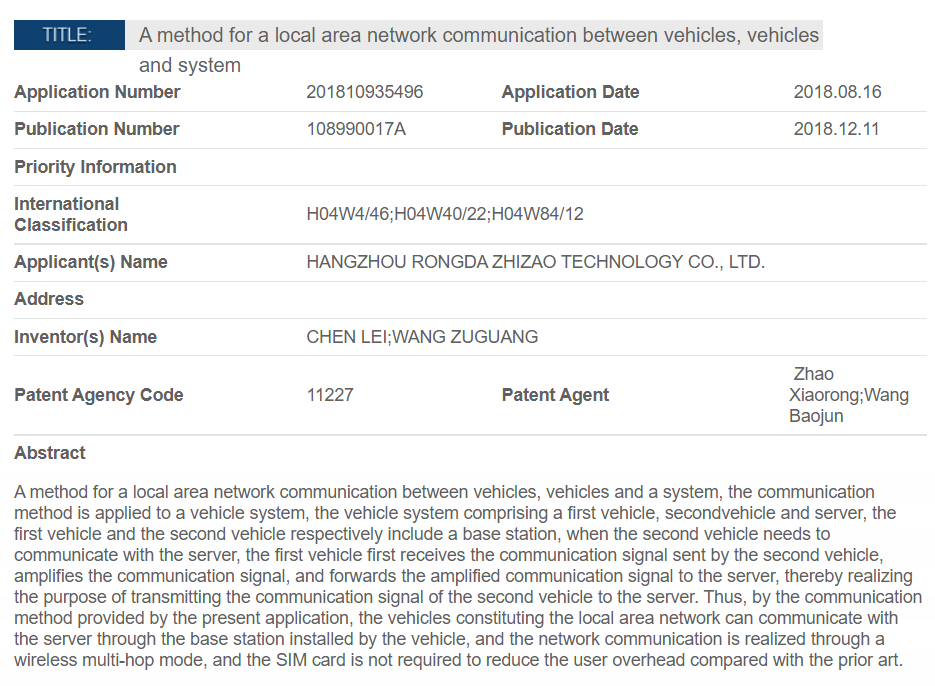

Of interest is this patent for network communication between vehicles:

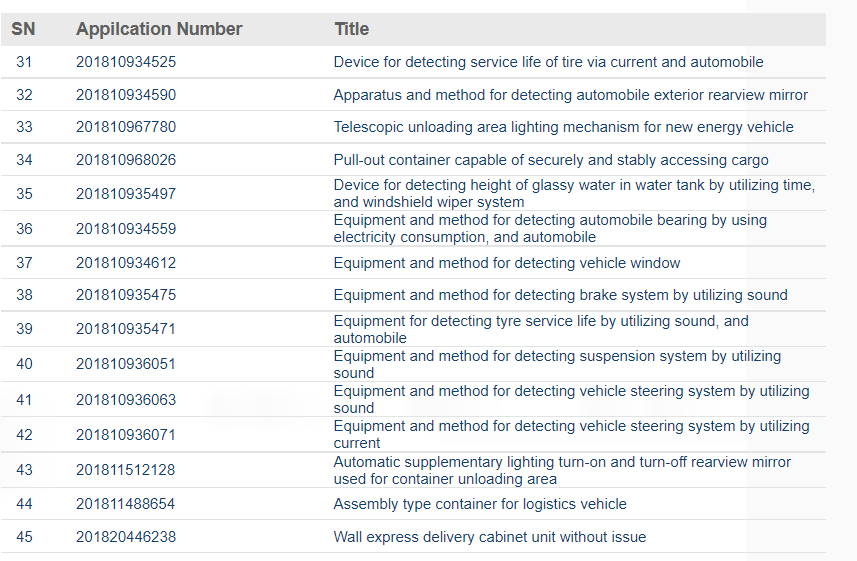

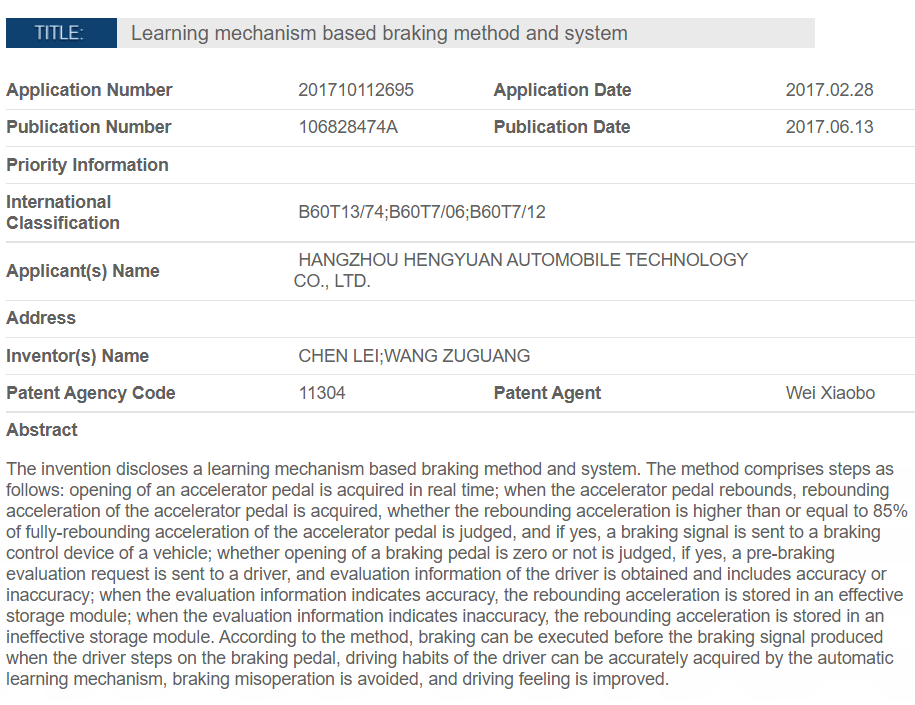

Hangzhou Hengyuan Automobile Tech has 61 patents. Skipping the screenshots of all of them. They have developed some sort of machine learning braking system:

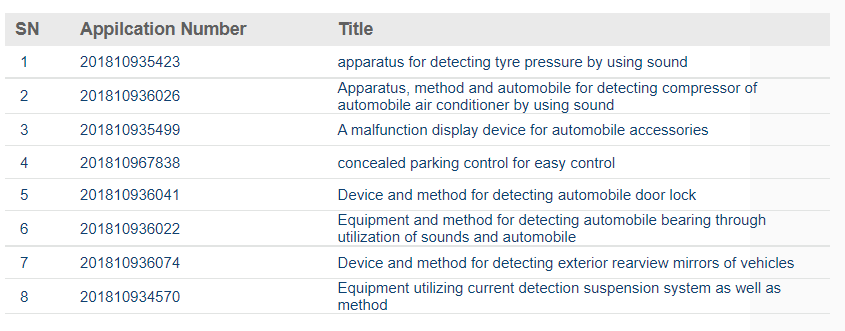

And whatever this is:

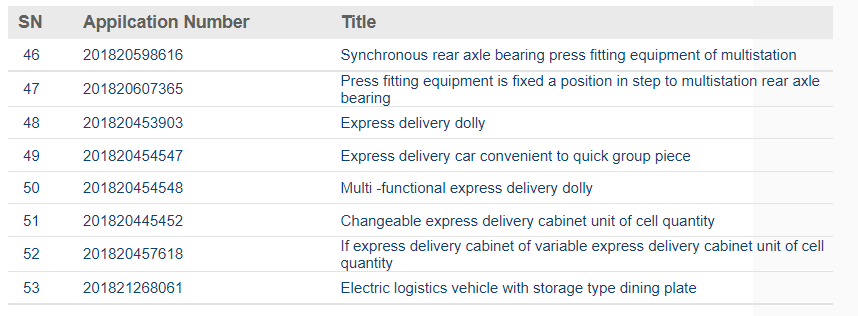

Rongda Intelligent Manufacturing has 8 patents:

Shengzhou Cenntro Machinery Co has three patents:

Notable that none of these patents are from later than 2018. No self-driving, automated intelligence, cloud computing, or chips to be found. Cenntro claimed to have developed a working prototype of the self-driving “smart chassis” in 2018, which does not seem to exist anywhere in the real world.

Update 12/30: Found a demo video of their self-driving chassis on YouTube, uploaded three months ago. The car can barely drive in a straight line and travels a total distance of about 100 feet. I still believe this technology does not exist and will not have commercial applications anytime in the near future.

Like the United States, China publishes patents 18 months after their application. It could be possible that Cenntro has made massive technological advances over that time period. That would require spending money on research and development, though.

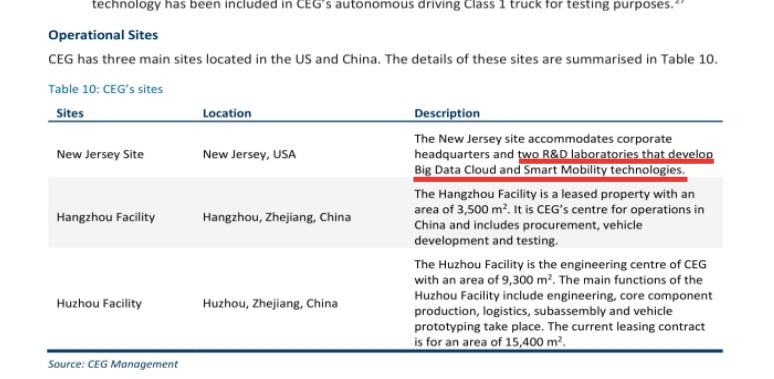

2.2 + 1.4 - .6 - .6 = $2.4 million in actual R&D over the last two years. The company alleges to have spent $74 million on R&D since inception. I would love to see proof of that. Cenntro has recently opened two “R&D laboratories” in Freehold, NJ

This is one of the facilities in Freehold, NJ:

Looks like a lot of “big data cloud” and “smart mobility technologies” are being developed there.

According to Cenntro’s LinkedIn, 6 of the company’s 17 employees are located in the United States. 0 of them have any title related to R&D, technology, engineering, etc.

Lawsuit

One more fun thing I found. Less than one year into Cenntro’s existence, Peter was advising another EV startup called KLD Energy. KLD was developing electric motors and established a partnership with Cenntro to collaborate on vehicle production. One of KLD’s investors, Benjamin Williams, filed a lawsuit in the Travis County, Texas District Court in November 2016. In the lawsuit, Benjamin alleges that he was defrauded by Peter Wang and KLD executives when he loaned the company money in 2012. You can read the full complaint here.

Peter was brought on as an advisor to KLD as an advisor to help the company start production in China and raise capital from investors. Williams says that he was shown an investor presentation that alleged Sinomachinery (another company Peter controls), was going to invest in KLD’s debt offering and partner with KLD in China for their production. with production in China. Williams was solicited to invest in this debt deal by Brian Okonsky, CEO and founder of KLD, and Peter. Williams ended up investing over $300,000 based on false information given to him by Peter and KLD executives. The form of the investment was a promissory note issued by KLD. Peter executed a guaranty on behalf of Cenntro for Benjamin on said Note. Over the next year, Williams was paid interest, but was asked multiple times to make additional investments into KLD or delay his receipt of interest payments, because KLD was always “on the verge of a breakthrough.” KLD started missing interest payments, and the company filed for bankruptcy in 2016. Williams initially sued Cenntro seeking to enforce the guaranty. Cenntro failed to appear, and Williams was awarded damages.

“Subsequent post-judgment collection efforts and investigation of Cenntro and Wang indicate that Cenntro is not and has never been in fact a functioning entity, nor has it ever had assets sufficient to cover the various debts Wang had accrued allegedly on its behalf, nor any intent to satisfy such obligations.”

In the suit, Williams made other strong allegations about Peter and Cenntro:

“It is now known that Cenntro is a sham entity, concocted by Peter Wang to defraud KLD’s investors and creditors. Cenntro is and has been at all relevant times undercapitalized and without separate books or accounts. Cenntro’s finances are not kept separate from Wang’s finances and his individual obligations are paid by Cenntro (and payments made to “Cenntro” were made by and for the direct personal benefit of Wang), Cenntro was used to promote fraud or illegality, and Cenntro did not and does not follow corporate formalities.”

The lawsuit was settled out of court.

Shareholders

Like many other stocks involved in the Great Short Squeeze of 2021, NAKD has gained a loyal shareholder base of retail investors. Peter clearly knows how to play to this:

"We looked at many options for going public," said Peter Wang, Cenntro's Chairman and Chief Executive Officer. "While we confidentially submitted a draft S-1 to go public via an IPO, we came to believe that Naked allowed us to go public faster, providing the working capital to support our substantial backlog. However, beyond capital, we felt the opportunity to gain such a loyal and enthusiastic shareholder base, such as the "Naked Army" and its other shareholders, was something that no IPO could achieve. We look forward to sharing many exciting developments in the coming months as we scale our deliveries."

go fuck yourself lol.

Conclusion

I think the SEC should have maybe done their job here. Naked Brand’s management and board have been either been negligent on the acquisition of Cenntro or intentionally withheld information from their investors. Cenntro and Peter Wang have lied about the company’s financial position, among other things.

$NAKD is supposed to start trading on the NASDAQ on December 30th, so I will be keeping my eye on that. It may be hard to short here because the shitco-$0 revenue-ponzi-“growth” sector has been beaten to shit over the past 6 months. Also I cannot get a borrow currently.

P.S.

As a private company, Cenntro was most likely not required to file financials with Hong Kong’s Registry System. But it sure would be a shame if the company happened to, and it would be even more of a shame if someone was able to purchase their documents. I tried to do this, but my card issuer did not like me trying to buy something from a Chinese government website, and declined the transaction.

I will probably follow up on this in the coming months if the SEC does something (wishful thinking) or when Cenntro begins to file official financials as a public company. Thank you for making it this far, and feel free to reach out via the comments here, my email, or on twitter with any feedback, questions, or comments.

Disclaimer: I am not Jacob Wohl. I am not 17. Please don’t sue me. I am not an investment advisor, and nothing in this article constitutes investment advice. I may or may not have positions in any securities mentioned in this article. This is not a solicitation to buy or sell any securities. Do your own research or call your advisor before making investment decisions. To the best of my ability and belief, all information contained herein is accurate and reliable, and has been obtained from public sources I believe to be accurate and reliable, however, such information is presented “as is,” without warranty of any kind – whether express or implied.

I followed your financial advice and sold all my CENN stocks. If you are wrong, I will sue you for my loss!!!

You’re a dumb ass!